We often hear about how hard it is to change the course of large ships, and as an analogy our current economic system seems to be hard to turn away from its course of counter-sustainability. However, large tankers DO make it into port. I would like to offer the idea that our economy can change course too. As with large ships, we need to understand and master the controls. Very few talk about accounting and sustainability. That is a shame, as several built-in features (and some easy to build in) could offer a way to turn the economy around. It’s not rocket science and it would be a big leap forward!

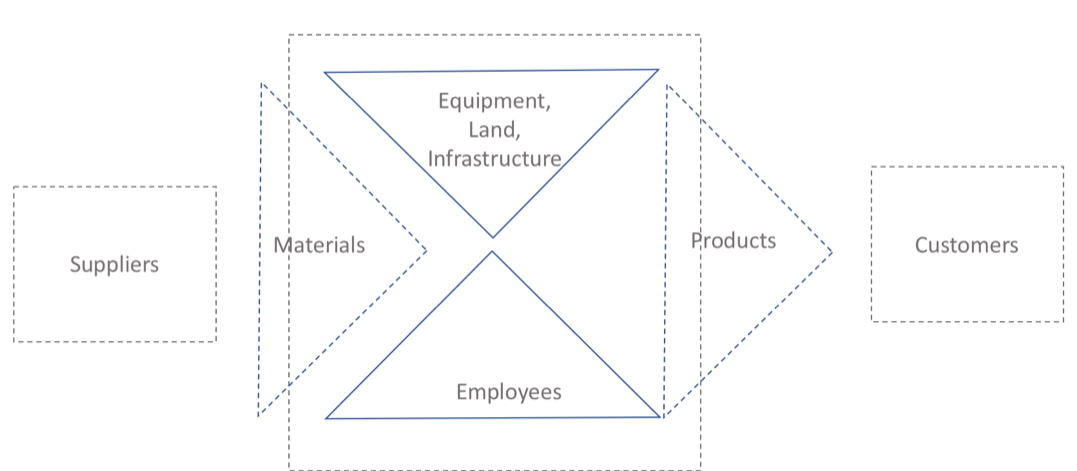

For those of you who are into sustainability but not accounting let me offer a simple model of the firm.

As you see in the diagram above, working backwards, customers pay for services, the money goes to the firm after delivery. The money compensates workers and pays for the inputs needed.

In order to start production there needs to be some kind of tools, machines, infrastructure set up and already in place. The money from sales goes to compensate those who put the money up.

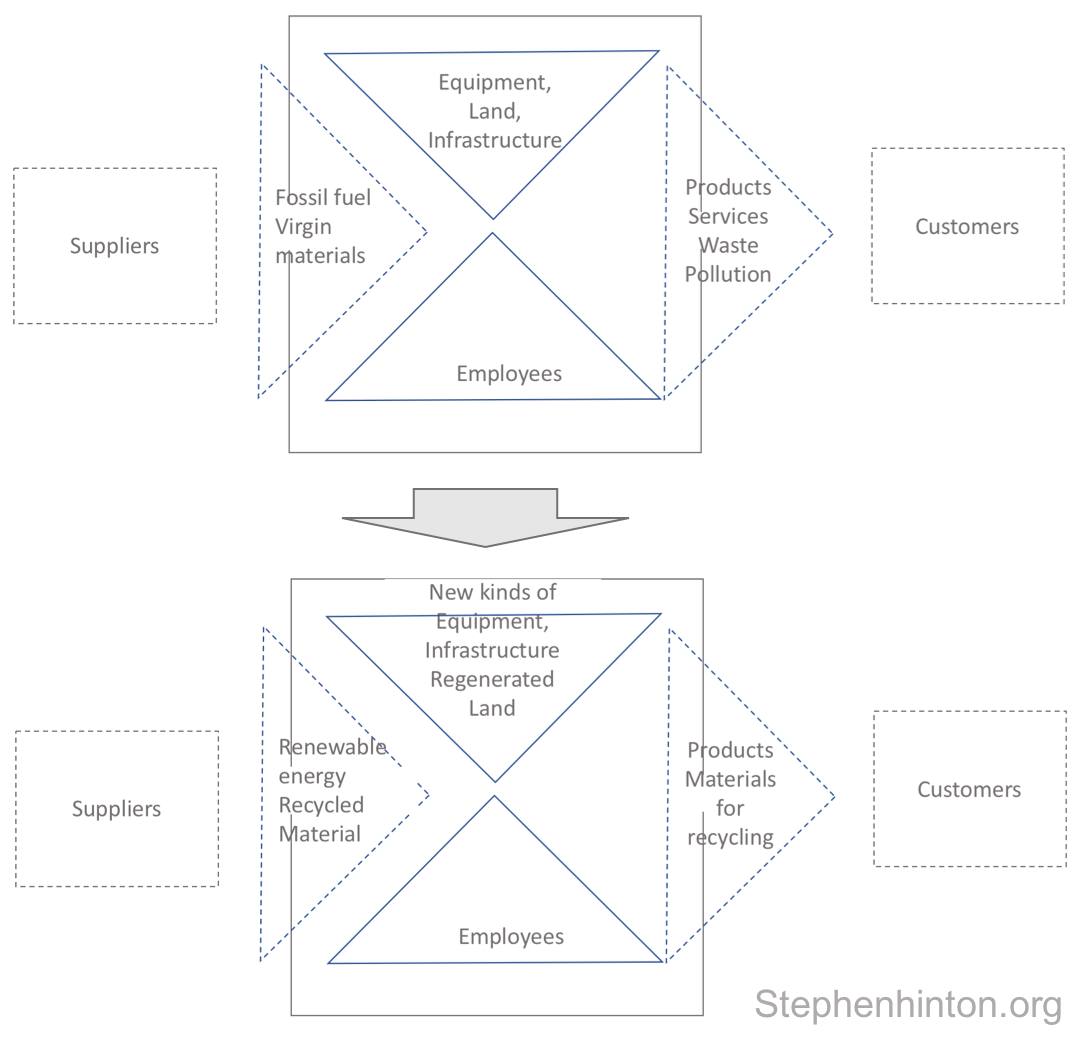

The firm of today needs to transform as the diagram below shows.

What is input into the firm needs to be recycled and renewable energy-based. This means new infrastructure, or at least adapted.

It also means that money spent on waste removal can be used elsewhere, and emissions will be zero.

To reflect this transition you need to adapt the way you do the accounting.

One advantage of bringing circularity into the balance sheet is that it becomes apparent how far the firm is along its transition. And it also illustrates the firm’s resilience to changes in regulations. These figures are invaluable to investors, owners and consultants all looking to prepare the firm for the fossil-free, circular future.

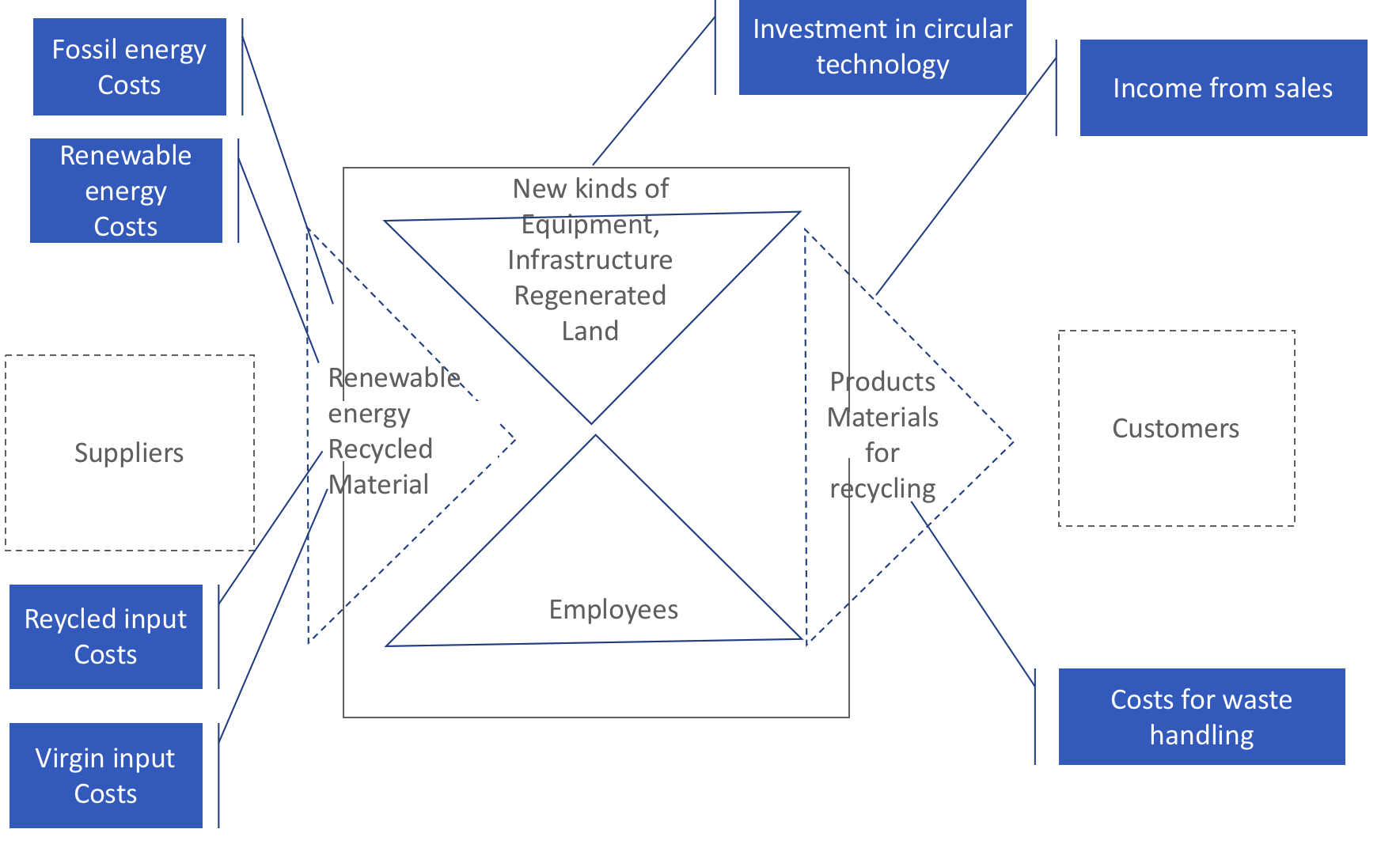

This diagram below explains where the various circular items come into the balance sheet.

In the fictive example below, the firm has more products that are linear than circular, but is on its way to becoming a circular enterprise. More has been invested in circular infrastructure for example, and profits are better on circular products.

| Revenue | ||

| circular products | 400,000 | |

| linear products | 600,000 | |

| Cost of goods sold

Energy |

||

| -renewable | 16,000 | |

| -fossil | 24,000 | |

| materials | ||

| -circular | 100,000 | |

| -linear | 200,000 | |

| waste handling | 1,000 | 30,000 |

| Gross profit | 283,000 | 346,000 |

| Operating expenses | ||

| Sales | 90,000 | 200,000 |

| Interest | ||

| -on circular investments | 30,000 | |

| -on linear investments | 20,000 | |

| Depreciation | ||

| Operating income | 193,000 | 126,000 |

| Interest income | ||

| Net earnings before taxes | 193,000 | 126,000 |

| Income tax expense | ||

| Net income | 319,000 |

MORE READING

- Follow this link to the fuller explanation of circular economy accounting

- To pull this off, the accounting needs to be accompanied by tighter regulations. The key is understanding the entry and exit points

- More about the changing nature of the firm

2 thoughts on “OPINION: Accounting needs to adapt to the circular economy”

Comments are closed.